Using your mortgage for debt consolidation

According to the Federal Reserve Bank of New York, Americans have a total credit card debt of $925 billion. That’s up $38 billion compared to the first quarter of 2022. This doesn’t include student loans, auto loans, or medical debt. Couple that with rising inflation, and Americans are looking for ways to reduce the amounts they owe and their monthly payments.

What is a debt consolidation mortgage?

A debt consolidation mortgage is a strategy to reduce your overall monthly payment, pay off debt faster and lower your number of monthly payments. At closing, or shortly after, those other debts are paid off, which leaves you with fewer loans and your new mortgage payment.

How does a debt consolidation mortgage work?

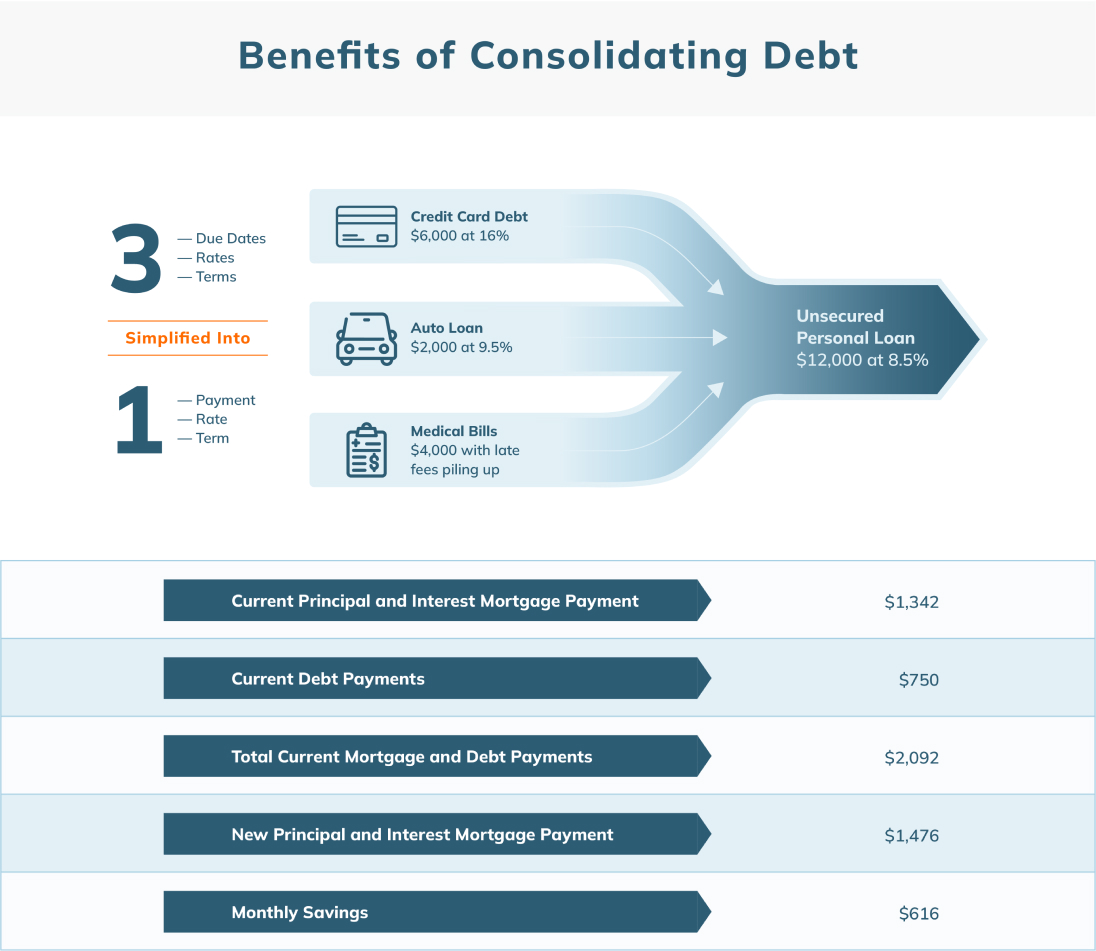

A debt consolidation mortgage works by taking payments from multiple debts (which typically have higher interest rates) and combines them into one payment. Usually you do a debt consolidation type of loan to help lower your overall monthly payment.

Usually, unsecured debt has a higher interest rate than secured debt. Unsecured debt is any debt that doesn’t have collateral attached if you default (personal loans, credit cards, etc.). Because there’s no collateral to collect if the borrower defaults on the loan, it is more risky for lenders, so lenders charge a higher interest rate. A secured debt has collateral attached to it (home, car, boat, RV, etc.). Which means the bank can recoup some of their costs if the borrower does not repay the loan. These rates usually have lower rates compared to unsecured loans, because they are considered less risky for lenders

For example, a borrower has $20,000 in credit card debt they want to pay off. They’re tired of paying that high 20% interest rate. That’s a monthly payment of around $400. Their current home is worth about $300,000 and has a balance of approximately $160,000 with a monthly payment of about $1520.

By doing a mortgage consolidation loan the lender would pay off the credit card debt, and a new mortgage would be created for $180,000 with an estimated monthly payment of $1697. So, while the mortgage increased by $177, it saves the borrower $223 a month overall.

Types of debt consolidation mortgages

There are several different types of refinances available to consolidate debt. Your personal financial situation will determine what option is best for you.

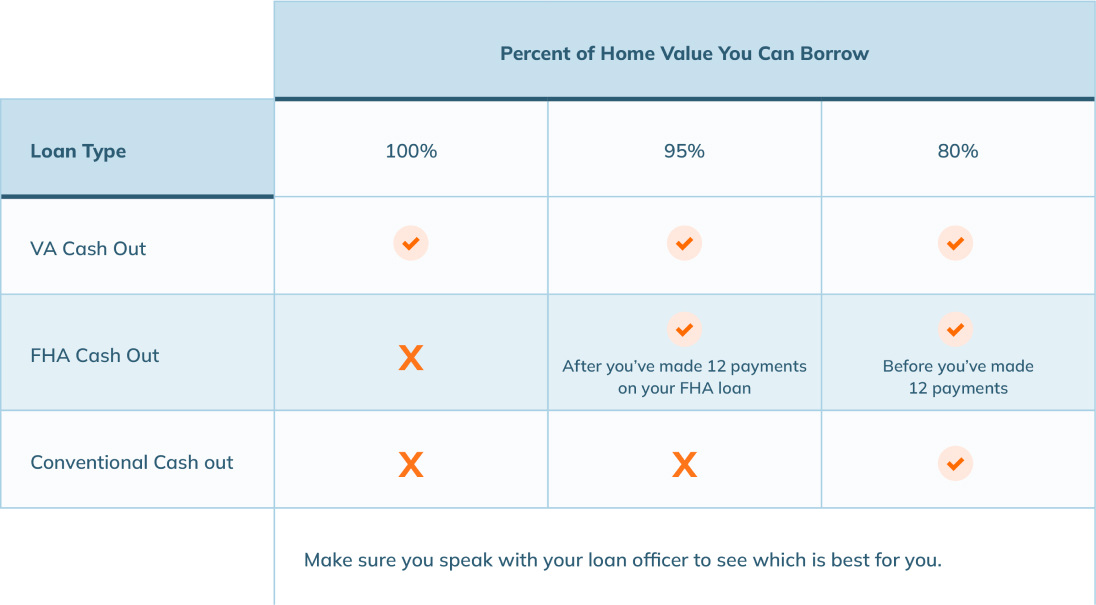

Cash Out Refinance

Borrowers can refinance their home and borrow some of their home value. Depending on your financial situation, you may qualify for a Conventional Cash-Out Refinance, FHA Cash-Out Refinance, or a VA Cash-Out Refinance. Each refinance option will have different requirements and limits for how much you can borrow against the home.

Home equity loans

Sometimes called a second mortgage, this is an additional loan against your home’s value. This loan is on a fixed rate and usually has a defined term (length) of the loan. You’ll receive these funds in a lump sum payment.

Home equity lines of credit (HELOC)

A home equity loan or home equity line of credit (HELOC) is where you borrow money from the equity in your home. You can use it similarly to a credit card, borrowing money when needed and then paying off the balance. A HELOC usually has a variable interest rate, so your payment will fluctuate depending on current interest rates in the market.

Reverse mortgages

Older homeowners have a record $11.12 trillion in equity in their homes. A reverse mortgage might be a good option if you’re over 62 years old and have a lot of equity in your home (over 50%). Payments don’t need to be made while you live in the home. However, your loan balance will grow each month due to fees and interest. Funds can be dispersed as a lump sum, monthly payments, or as a line of credit.

Pros and Cons of a Debt Consolidation Mortgage

Debt consolidation can be a great option to help streamline your finances if you’re dealing with multiple debts or want to simplify your payments.

The pros of debt consolidation

- Lower interest rates – Because it is a secured loan, you’re more likely to get lower interest rates than your unsecured debt. Borrowers could go from a 20% interest rate on a credit card to a 6% mortgage rate.

- Single monthly payment – Instead of making payments to three or four different lenders on your debt, you’re making a single payment to one lender now. Thus making it easier to keep track of who’s been paid and who hasn’t.

- Possible tax benefits – There could be tax benefits on rolling over your debt into your mortgage. However, the IRS rules about deducting mortgage interest payments can change, so be sure to check and verify the latest rules.

- Fixed end date – Because a mortgage is usually on a fixed term (15 or 30-year terms), they have a fixed end date. You’ll know how long you’ll be paying on the loan.

The cons of debt consolidation

- Longer repayment period – Because the term for a mortgage is usually 15 to 30 years, you’ll be paying on your debt consolidation for a long time.

- Your home is attached – If you fail to make the payments, your home will be foreclosed on.

- Good credit requirements – The best terms are still given to those with the best credit. So if you’ve already missed payments and your credit has been hurt, you’re more likely to get a higher interest rate.

- Closing fees are still around – Because this is another loan process, costs and fees to close the loan are involved.

- You may still have access to get back in debt – Certain debt types, like credit cards will still be available to use unless you cut off your access to them. If you are likely to run up your balance on your credit cards even after a debt consolidation loan, you should strongly consider cutting up your card.

Alternatives to a Debt Consolidation Mortgage

If you’re worried about using your home as collateral as part of your debt consolidation plan, there are several alternative ideas you might look at.

- Personal Loans – A personal loan allows you to consolidate your debt and start paying that off. These are usually smaller amounts and are unsecured loans. They have a higher interest rate than a mortgage or car loan but generally have lower interest rates than a credit card.

- 401(k) loan – You might be able to borrow from your retirement fund. You’ll have to repay the amount you borrowed, and you’ll have five years to pay it back. While it might be beneficial in the short term to do this, there could be some long-term consequences.

- Balance transfers – Some credit cards offer a 0% interest period for balance transfers for 12-18 months. This allows you to transfer your credit card debt from one that has a high-interest rate of 16-25% to one with 0% for an extended period. By not having to pay interest and paying directly to the principal, you can quickly make a dent in your debt.

- Debt management plans – Third-party companies can help you manage your debt. They have specialized plans to help you create better habits and have the resources to work with creditors to possibly lower your monthly payments.