Congrats! SqrdMedia Loves You.

SqrdMedia has partnered with us to get you access to instant quotes, below market interest rates on purchases and refinances, and a $500 Visa Gift Card at funding—just to name a few—all for free!

- No personal information required

- No upfront deposit for appraisal or credit report required

- Expect to save money

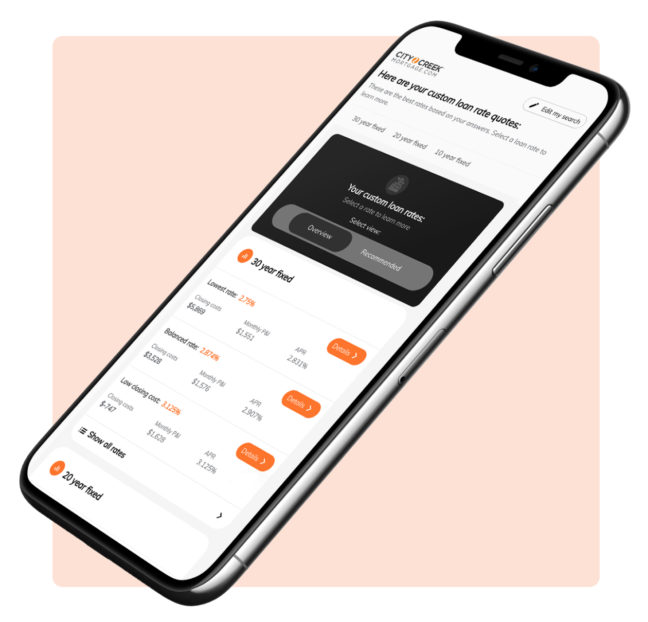

Today’s Rates

30 Yr Conventional Fixed

1.525 points

What are mortgage points?

What are mortgage points?

Purchasing mortgage points is essentially prepaying interest to the lender, which allows you to secure a lower interest rate for the life of the loan.

Not sure if you should pay points? Don’t worry. You don’t have to decide until a few days before closing.

What are mortgage points?

What are mortgage points?Purchasing mortgage points is essentially prepaying interest to the lender, which allows you to secure a lower interest rate for the life of the loan.

Not sure if you should pay points? Don’t worry. You don’t have to decide until a few days before closing.

6.125%

Interest rates

This is the interest rate applied to your home loan, and directly affects your monthly payment. Locking in a competitive rate can help you save on interest, and make homeownership more affordable.

Interest ratesThis is the interest rate applied to your home loan, and directly affects your monthly payment. Locking in a competitive rate can help you save on interest, and make homeownership more affordable.

APR 6.308%

APR: (Annual Percentage Rate)

The total cost of your mortgage, including interest, lender fees, and other charges. Since lenders can pick and choose what is included in this calculation, it’s not the best way to compare.

APR: (Annual Percentage Rate)The total cost of your mortgage, including interest, lender fees, and other charges. Since lenders can pick and choose what is included in this calculation, it’s not the best way to compare.

Lowest rate, highest upfront cost

Check Closing Costs

0.721 points

6.375%

APR 6.483%

Low rate with upfront cost

Check Closing Costs

-0.137 points

6.625%

APR 6.664%

Balanced rate and upfront costs

Check Closing Costs

-0.830 points

6.875%

APR 6.882%

Lowest upfront cost

Check Closing Costs

Rates as of July 3, 2025 See Rate Assumptions

Customize your rate in just 60 seconds

What's Included

Free benefits for you.

$500 Visa Gift Card

Upon funding, you will receive a $500 Visa Gift Card

Zero upfront & application fees.

It costs nothing for you to explore potential savings. With no application fees, you have nothing to lose!

Low interest rates & fees.

Lower rates means more money for each of you.

Salary-Based Loan Officer

Your best mortgage doesn't include high-pressure, high-commission sales people.

$5,000 close on time guarantee

Don’t want to miss that closing date? We get it! We guarantee to close your loan by the date stated in your contract. If we don’t, we’ll write you a check for $5,000.*

… Did we mention more happiness?

Wondering what it's like working with us? We got you.

Testimonials

2,752 people can’t be wrong

2,752 Reviews | Average 5/5

Apply Now

You're about to save time and money going with City Creek Mortgage.

With zero up-front fees, you can explore how this program can save you thousands. We'll walk you through every step of the way. Take advantage now!

Benefits Coming to You